Everyone wants a crystal ball.

Since we don’t have one, we are relying on over 40 years of experience with hundreds of clients and our strategic partnerships to understand what’s coming for the family office industry.

In 2024 firms that serve Ultra-High-Net-Worth (UHNW) families are dealing with the complexities of generational wealth transfers, increased cybersecurity risks, staffing challenges, and the need to provide a better client experience to retain relationships.

Generational Wealth Transfer

Generational transitions are going to become a top concern for family offices for three reasons.

- When wealth transfers there is a risk that the next generation will not stay with the firm their parents chose. In fact, a report from Cerulli reveals that only 20% of affluent clients plan to stay with their parents' advisors. Historically the first or second generation of wealth creation establishes the relationship, but it’s rare that they bring the next generation into the room. To beat the odds, firms need to start these relationships earlier.

- This shift is going to require firms to meet the expectations of their new tech savvy clients. These clients expect firms to provide real-time, interactive information on demand. Younger clients expect firms to enable better decision making, answer their questions on the fly, and provide more proactive management. Family offices must be equipped to satisfy this range of expectations, with the flexibility to deliver reporting and communications through the preferred channel for each family member - whether that is email, text, or an online portal.

- This transition will also likely result in more accounting complexity, an increase in entities, and the number of bills family offices are responsible for paying. Implementing workflows and automation now will help your family office easily scale when more complexity is introduced.

Bottom line: To meet client demands firms will need to rely on technology to streamline operations, enhance client services, and to manage complex wealth more efficiently. AgilLink is helping family offices with our scalable and efficient bill payment process, mobile app, Application Programming Interface (API) integrations with Investlink and inAssist.

Increased Cybersecurity Risks

Considering the amount of wealth family offices handle, and the many touchpoints they have with various financial institutions, it’s not surprising that they are a likely target for hackers and bad actors. In the 2023 Campden Wealth North American Family Office Report, 21% of family offices reported experiencing one or more cyberattacks over the preceding year.

To protect families, firms need to focus on better safeguards around the privacy of information, by using technology that has strong authentication, and encryption built in. They also need to choose technology platforms that have the expertise and ongoing commitment to ensure the highest standards of security are met. Since this level of security is rarely available in retail products, firms should explore technology that is purpose built for the wealth management industry.

Staffing and talent challenges

Family wealth firms are finding it hard to attract and retain exceptional employees. This challenge will force them to rethink how they can better maintain employee satisfaction, productivity, and engagement. We know that happier employees help firms lower their costs of recruiting and onboarding. More importantly, happier teams foster better client service and relationships.

- Streamline Repetitive Tasks: No one enjoys manual and repetitive tasks. Integrating technology and software solutions with work-flow processes is critical to improving the day-to-day life of a family office’s staff. AgilLink prides itself on enabling firms to scale their business and make their bill payment and accounting services more efficient, and less labor intensive.

- Prioritize Work Life Balance: Many family offices have found that the key to preventing employee burnout is to offer a better work/life balance. This means prioritizing consistent work hours, providing breaks throughout the day, and encouraging wellness activities.

- Identify Issues and Opportunities Proactively: Another popular retention and recruitment effort is to conduct “stay” interviews. These informal check-in conversations take place every 6-12 months to discuss what they love about their role, and to uncover anything that could prevent employees from thriving at work. When done correctly, stay interviews can have an extremely positive impact on employee retention rates.

One often underestimated risk is relying too much on an in-house expert. This happens when the firm has one staff member tasked with completing manual tasks and dealing with the intricacies of reporting spreadsheets. In this situation, areas of expertise develop with one individual, which can leave the office in a lurch when the expert leaves. To avoid this risk, it’s important for firms to use transparent workflows and automation to streamline the operational process.

By adopting technology platforms and automating burdensome data management and reporting tasks, family offices find it easier to attract top talent and reduce turnover risk.

Creating Better Client Experiences

With increased competition in the family wealth industry, more firms are focusing on creating better client experiences (CX). This means providing personalized services, anticipating client needs, and exceeding their demanding expectations.

To deliver an exceptional client experience firms need to consider how to:

- Offer services that meet the needs of the family. Firms need to align their services with the specific needs and preferences of each family, delivering bespoke offerings that address their unique requirements. The first step is to segment your clients by their distinct need. For example, if a family member has a passion for art, your office can provide services to invest in alternative assets, and a partnership with an art expert to help your clients identify opportunities. Another example is if a family member is diagnosed with dementia, your office can step up and handle all their day to day finances, including their bill payments to alleviate concerns that something will be missed.

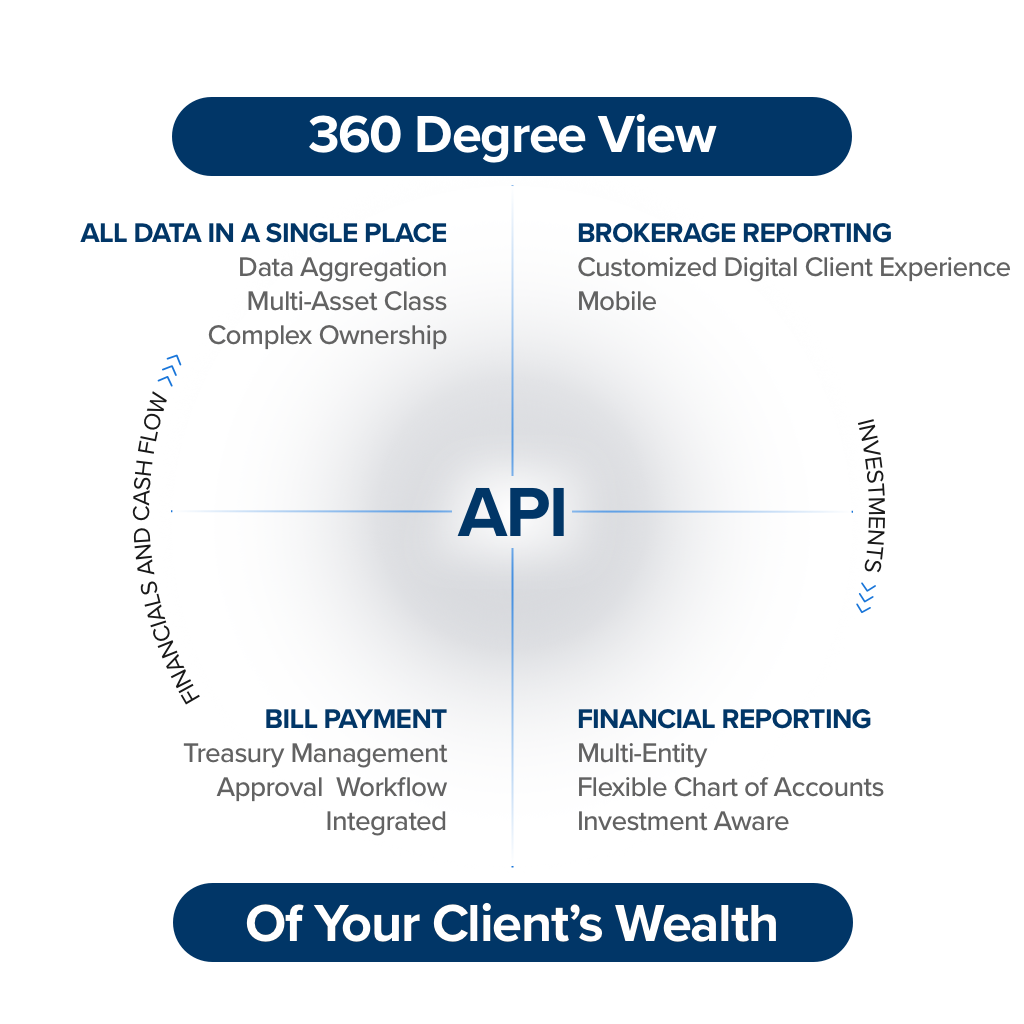

- Provide accessibility, transparency and on demand reporting for better decision making. To remain competitive, firms must leverage technology to enhance accessibility, provide real-time data, and streamline communications with families. Firms face significant challenges when it comes to turning data from disparate systems into key insights for clients. Successful firms require a comprehensive view into a variety of data, including: financial data to support decision-making, portfolio data on asset allocation, and continuous monitoring of processes to mitigate risk. Many firms have found that that is easier said than done, because they are stuck working with an outdated and siloed technology stack. With AgilLink your team gains that true 360 degree view of a client’s financial life, by having your general ledger integrated with your investment performance data. This integrated view allows the firm to provide more comprehensive reporting and arms advisors with a truly holistic approach to advice, tax preparation and better decision making.